FDA Breakthrough Device designation for mm.X plate system

Press Release

medical magnesium receives FDA Breakthrough Device designation for their bioabsorbable traumaorthopedic plate system based on mm.X magnesium implant platform

Jan. 11, 2023, 11:00 CET

Aachen, Germany, Jan. 11, 2023/ — medical magnesium GmbH, a Aachen-based medtech company creating bioabsorbable implants, announced today that the U.S. Food and Drug Administration (FDA) has granted the company Breakthrough Device status for their orthopedic and trauma care plate system.

„The Breakthrough Device designation for our bioabsorbable orthopedic plates recognizes our ability to address one of the biggest unmet clinical needs in orthopedic surgery and traumatology,” said Kilian Reuß, CEO and co-founder of medical magnesium. Routinely performed surgical removal of conventional implants is undoubtedly a major burden for patients, especially in pediatric surgery. The bioabsorbable plate system will eliminate this burden and reduces the total costs of care significantly.

The mm.X plate system is currently under development and has shown tremendous potential in in-vitro and in-vivo tests. “The breakthrough device designation allows us to regularly synchronize our development process with the FDA and to clearly meet the patients‘ and physician‘s requirements for safe and well-

performing medical devices early on. The on-going collection of promising clinical data on other products of the mm.X family currently marketed in Europe further enriches the exchange with the FDA greatly.” Dr. Michael Gertig, VP Regulatory & Clinical Affairs

About medical magnesium

medical magnesium is a medtech company for bioabsorbable implants based in Aachen, Germany – founded in 2018 by Florian Coppers, Kilian Reuß from RWTH Aachen University. The high-tech company offers a wide range of CE marked bioabsorbable magnesium implants in Europe to a growing number of orthopedic surgeons recognizing the need for a single surgery therapy the and value for their patients. medical magnesium seeks to provide this kind of treatment to American patients soon.

About the FDA Breakthrough Device Program

The FDA Breakthrough Device program enables expedited regulatory assessment of novel technologies with the potential to provide more effective treatment or diagnosis of life-threatening or irreversibly debilitating diseases or conditions. The goal of the Breakthrough Devices Program is to provide patients and health care providers with timely access to these medical devices by speeding up their development, assessment, and review, while preserving the statutory standards for premarket approval, 510(k) clearance, and De Novo marketing authorization, consistent with the Agency‘s mission to protect and promote public health.

Contact

Kilian Reuß

Medical Magnesium GmbH

Philipsstraße 8

52068 Aachen

info@medical-magnesium.com

+49 241 927845023

Related Links

Training of clinical trial investigators

When developing novel and innovative medical devices, it is usually necessary to actively generate safety and performance data on patients. These data are generated in clinical trials and are required to demonstrate compliance with regulatory requirements. The safety of a medical device depends on product related risks and on the complexity of its application. The more complex the application of a device, the greater the associated risk. While device-specific risks are addressed during design development, application risks are minimized by user training during clinical practice. Because the safety of participants is of highest priority in a clinical trial, investigators should already gain experience with the investigational device and acquire a certain routine in its use prior to enrolment of the first study subject.

Investigator training

The use of magnesium implants does not require any special surgical procedure or method that deviates from the clinical standard. However, the mechanical properties of magnesium alloys differ from those of titanium or stainless steel. Thus, mm.X implants such as the mm.IF interference screw or the mm.CS compression screw demonstrate unique insertion behavior and specific mechanical load capacities. Before treating the first patient in a clinical trial, investigators should already be familiar with the mechanical properties and the correct handling of mm.X implants and instruments. This requires training under the most realistic conditions such as the implantation of mm.X on human specimen. As part of each clinical trial preparation, we therefore arrange investigator meetings with training sessions at the Cadlab Cologne, a top-class training facility for the surgical education of physicians on freshly frozen human specimens. Apart from the training, we use the meetings to discuss the most important points of the studies and offer all study investigators the possibility to interact and to get to know each other.

Insights from mm investigator meetings

The first part of each investigator meeting is used to present the clinical trial to the investigators (see Figure 1, right picture).

Figure 1: Explanation of study activities during the mm.IF investigator meeting at Film Studios CadLab Cologne.

During this session, investigators can give input and discuss open questions while considering the foreseen measures for data collection, eligibility criteria for study participants, visit plans as well as objectives and endpoints of the study. The session is shared online to allow virtual participation of investigators who cannot attend in place. The investigator meetings are carried out prior to finalization of the study protocol and approval by ethics committees and competent authorities. Thus, it can be ensured that the results of the discussions are adequately considered for the clinical trial.

An introduction into the second session is given by our product manager who presents the available specimen, the surgical procedures, and the mm.X implants that are relevant for the clinical trial. This is followed by mm.X training on human specimen. Always two operation teams can work simultaneously on separate specimens to minimize waiting times. Investigators choose the surgical procedure, the required device configuration and perform the mm.X implantation, similar as done during regular practice and in the clinical study. After each surgery, the results are visualized by X-ray imaging and discussed together. At any time, medical magnesium staff is available for questions, suggestions, and hand-on support for the surgeon (see Figure 2). This offers an optimal environment for investigators to familiarize with the implants, the available configurations and the instruments intended to be used in the clinical trial. Like the first session of the event, also the surgical training session is shared online. This allows all investigators, who cannot attend in place, to participate, to ask questions and to give input any time.

Figure 2: Impressions of the mm.IF study investigator training at Film Studios Cadlab Cologne.

In the third and final session of the event, investigators have the possibility to check out the mm.X portfolio independent from the clinical trial (see Figures 2 and 3). What kind of surgery and implants can be applied depends on the human specimen available, e.g., an isolated foot or an entire leg. Interference screws (mm.IF), compression screws (mm.CS) and implants for forefoot surgery (mm.PIP) are available. Usually, investigators use this session to test mm.X implants they have no experience with, and to practice new or unfamiliar surgical procedures to improve personal skills. In all cases, the results of the surgeries are visualized by X-ray imaging and provided to the surgeons afterwards.

Figure 3: Testing session (left) and closing of the mm.PIP investigator meeting (right) at Catlab Cologne.

Conclusion

With the help of study-specific and realistic training events, investigators are adequately trained on mm.X implants, available device configurations and instrument handling prior to trial initiation. This measure ensures the safety of the study participants in the best possible way.

Green logistics

In our modern world the increase in air pollution, global warming, environmental issues and degradation has become a significant matter of concern not only for modern businesses but also for societies and governments. Consequently, Green Supply Chain Management (GSCM) is moving more and more into the focus of attention of society and businesses. But before we go into more detail, we should take our time to define what a green supply chain is and how we can create it.

Definition

GSCM is a diverse concept but by breaking it down to the core, it is the principle of reducing waste by increasing efficiencies. Therefore, GSCM is all about delivering products and services from suppliers to clients through material, cash and information flow in the context of environment. Effective management of suppliers and resources is a crucial part of GSCM. GSCM adds a new ecological layer to each and every stage of crafting and service and increases awareness and concern among people and businesses about climatic factors.

Benefits of creating a green supply chain

- Enhancing brand image: Businesses that consequently follow the ecological road of GSCM will find that it does enhance the brand imagine and reputation in a customer’s ‘mind

- Transparency of the supply chain: By implementing the ecological aspect to every step of the supply chain, businesses often become more transparent to customers, which also boosts the brand imagine, as mentioned earlier

- Competitive advantages: Among many other factors, recent researches have shown that roughly 6 percent of leading companies already deselect suppliers who fail to manage carbon (1)

- Cost reduction: By implementing digital technologies, businesses will financially profit from it. A prime example for cost reduction is reducing unnecessary kilometres by switching to local suppliers if possible and reasonable

Challenges of creating a green supply chain

- The Akerlof effect: George A. Akerlof has shown that there are issues that arise regarding the value of a product due to asymmetric information possessed by the buyer and the seller (2) In this case buyers cannot distinguish between a high-quality car and a “lemon”. Therefore, they may not be willing to pay no more than the average price. The seller on the other hand knows the difference and knows whether he is selling a lemon or a peach. Given the fixed price at which buyers will buy, sellers will sell only when they hold lemons and they will leave the market when they hold peaches. When enough sellers of peaches leave the market the WTP of buyers will slowly decrease leading to even more sellers of peaches to leave the market through a positive feedback loop

- Supplier compliance: In order to create a green supply chain, a company must procure its materials from other green supply chains. Therefore, we can say that the idea behind a green supply chain is based on the foundation of trust and good faith. The problem here is to get your suppliers to comply to your ideals (and this is usually near impossible in most cases)

- Monitoring complex supply chains: The bigger the company is the greater are their supply chains. Monitoring these supply chains will be very challenging, as a single product may have a myriad of different materials, suppliers and manufacturers along its supply chain. Furthermore, smart businesses employ several suppliers per piece to ensure continued delivery in case on supplier drops out

Going green?

Previously mentioned benefits, including competitive advantages & cost savings will, in the long run, become a pre-requisite for business sustainability. In the end, it is up to you to decide to change to a greener supply chain or to stick to the existing one. Whether to comply with government regulations or meet the expectations of the customers or clients, businesses are finding motivation to go green. (3)

Green supply chain at medical magnesium

For our supply chain area, we take many arrangements to make the transport of products as green as possible. The sustainability strategy will be constantly optimized and the process will be adapted by further measures in order to come as close as possible to absolute green transport.

A first starting point for medical magnesium is the recycling and reuse of packaging materials.

Why consume new valuable resources for something that will only be thrown away?

Recycled paper products, cardboard boxes, filling material, etc. are partly designed to be used more than once, so packages can be perfectly packed without unnecessarily wasting resources.

Furthermore, we rely on recycled materials when it comes to padding. For the protection of the goods fiber boards from the company Biobiene (FSP Full Service Packaging) are used:

Figure 1: Fiber Boards

The protective fiberboard protects sensitive shipping goods by resilience and shock absorption. Since they are made of environmentally friendly and easy disposable 100% post-consumer paper, they can be returned to the waste-paper-cycle after use. (4)

In order to get closer to „green shipping“, in the future plastic document pouches will be replaced by paper delivery note pouches. The used paper grades are bleached without chlorine and meet the sustainability criteria of forest management in accordance with FSC and PEFC standards. This adhesive not only provides a firm hold on transport boxes but is also particularly environmentally friendly. (5)

Our supplier has been awarded the sustainability prize of the German Brand Award. In addition to the German Brand Award, we obtain our shipping products from a supplier who has achieved the highest distinction of the German Brand Award „Best of Best“ Sustainable Brand of the Year 2018. (6)

For the protection of our implants, we use foam inserts made from recycled PE-foam with CO2-neutral production. The foam is made from recycled and shredded foam leftovers and creating a closed recycling loop. The PE-LD recycling system is connected to a photovoltaic system, so that production and manufacturing take place with climate-neutral solar energy. (7)

Figure 2: Custom made PE-foam inserts for implant protection

Even changing small factors within the supply chain can have a big impact. That’s why we use paper tape from Naturapack GmbH instead of conventional adhesive tape. The paper tape has an adhesive layer made of environmentally friendly natural rubber and is therefore free of plastic. (8)

In the future, we will dispense with the classic plastic air cushion bags for cushioning the spaces between the goods and instead rely on a paper cushioning system. Natural and environmentally conscious paper pads are an optimal and efficient protection for packaging.

Figure 3: Paper cushioning system

In addition to green shipping, we also set focus on the sustainable production of our implants. Through continuous monitoring and education, we can identify processes to make sustainable adjustments or replace with greener alternatives.

In some places, unfortunately, our hands are tied, when it comes to our material, since these implants out of the magnesium are still very innovative. But here, too, we keep an eye on the manufacturing processes in order to identify adjustment options as early as possible. However, we try to make the entire production as green as possible and are always on the lookout for more environmentally friendly alternatives.

We look for recyclable and sustainable products with minimal CO2 footprint, environmentally friendly packaging, and responsible life cycle when it comes to supplier selection for the packaging system so that our supply chain aligns with regulatory and corporate sustainability goals.. We are happy that our mm.x implants make a sustainable way to our customer and hope to support sustainability within the supply chain to create awareness and transparency with our blogpost.

References

- Sheffi, Yossi. „Clarifying The Business Case For Green Supply Chain Management.“ 13 June 2018, www.inboundlogistics.com/cms/article/clarifying-the-business-case-for-green-supply-chain-management/. [Accessed 14 June 2022].

- Akerlof, George A. (1970). „The Market for ‚Lemons‘: Quality Uncertainty and the Market Mechanism“. Quarterly Journal of Economics. The MIT Press. 84 (3): 488–500. doi:10.2307/1879431

- Bomler. “3 Challenges of Sustainable Supply Chain Management [and How to Solve Them].“ 16 August. 2021, www.bomler.com/blog/3-challenges-of-sustainable-supply-chain-management-and-how-to-solve-them. [Accessed 14 June 2022].

- Biobiene – Faserplatte, [Online]. Available: https://www.biobiene.com/schutz-faserplatte-780-mm-x-380-mm-x-25-mm.html. [Accessed 13 June 2022].

- Biobiene – Lieferscheintasche, [Online]. Available: https://www.biobiene.com/verpackungsmaterial-gruene-lieferscheintaschen-aus-papier-din-lang?c=2030. [Accessed 13 June 2022].

- Biobiene – Award, [Online]. Available: https://www.biobiene.com/magazin/german-brand-award/. [Accessed 13 June 2022].

- Stephan Verpackungen, [Online]. Available: https://www.stephan-verpackungen.de/. [Accessed June 13 2022].

- Naturapack GmbH, [Online]. Available: https://plastikfrei-verpacken.de/produkt/kleben/papierklebeband/papierklebeband-weiss-50mm-x-50m-3-fach-faserverstaerkt/. [Accessed 14 June 2022].

Imaging of mm.X magnesium implants

Today, modern imaging techniques enable the production of high-resolution images and thus precise diagnostics and surgical planning. Postoperative images are commonly used to evaluate the correct placement of implants and to assess surgical success. Various imaging techniques are available, and which one is most suitable depends on the anatomical structures to be visualized and the implant’s material. Not every imaging technique is compatible with each (and every) implant material. Especially metal implants induce a variety of artifacts, which is a major problem with orthopedic implants. The following sections describe the functionality of X-ray, computed tomography (CT) and magnetic resonance imaging (MRI) and their suitability for imaging magnesium implants in orthopedic and trauma surgery.

X-Ray imaging

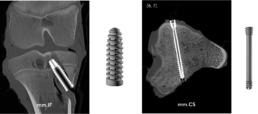

In this examination technique, X-rays pass through the tissue or object to be examined whereas the radiation is attenuated to varying degrees depending on the density of the tissue. The residual radiation emerging from the other side of the tissue is detected and converted into a two-dimensional projection (see Fig.1).

Figure 1: Ex vivo radiographic imaging of various magnesium implants in human specimens (left, interference screw; middle, PIP implant; right, compression screw). Images by [1] Jun.-Prof. Dr. med. Thomas Pfeiffer and [2] PD Dr. med. Daniel Günther, each Department of Trauma Surgery, Orthopaedic Surgery and Sports Traumatology, Cologne Merheim Medical Centre, [3] Dr. med. René Burchard, Clinic for Orthopedics and Trauma Surgery, Lahn-Dill Clinics (https://www.linkedin.com/in/dr-med-rene-burchard-mhba-73574612b), [4] Adem Erdogan, Specialist for Foot Surgery, Dusseldorf (https://www.linkedin.com/in/adem-erdogan-m-d-59846260).

X-ray examination is inexpensive and requires little effort. Therefore, it is widely used for various imaging purposes. However, a disadvantage of this technique is the superposition of objects in the two-dimensional projection, which can make it difficult to separate two objects with similar densities. For this reason, 3D X-ray is increasingly used in practice (1). Conventional X-ray technique is well suited for visualization of osseous structures and magnesium implants (see Fig. 1) and is therefore the basis of imaging follow-up after implant surgery. However, X-ray examinations are associated with radiation exposure.

Computed tomography (CT)

Computed tomography is a type of X-ray examination in which the radiation source and detector unit rotate within a ring around the patient. By moving the patient table through the center of the ring, the patient or object to be examined is penetrated by X-rays from several angles. As with conventional X-ray examination, the rays are attenuated to varying degrees depending on the density of the tissue. The measured radiation on the other side of the X-ray source is then converted by a computer into a three-dimensional stack of images with different gray values.

CT is suitable for precise visualization of osseous structures and surgical implants, as the images are characterized by a very high level of detail and excellent resolution. For this reason, the technique is often used for clarification diagnostics if a reliable delimitation is not possible using X-ray investigation (5). A major drawback is the formation of artifact at the interface of metal and bone or soft tissue. Artifacts are imaging errors resulting from the physical measurement principles that do not correspond to reality. They occur to varying degrees depending on the metal and, in CT, may be due to metal-induced beam absorption (hardening artifacts and the „photon starvation effect“) or photon scattering (scattering artifacts). If artifacts are located directly at the interfaces of implants and bone, it complicates the assessment of nearby pathologies markedly. Thus, individual optimization of the acquisition parameters is necessary (6). Implants made up by magnesium alloys induce artifacts only to a very small extent making them favorable for CT imaging (Fig. 2).

Figure 2: Computed tomography of ex vivo specimens containing magnesium implants (left, interference screw; right, compression screw).

Images by [5] Stephanie Tackenberg, Department of Diagnostic and Interventional Radiology, University Hospital RWTH Aachen, [6] Dr. med. Leona Alizadeh, Department of Diagnostic and Interventional Radiology, University Hospital Frankfurt (https://www.linkedin.com/in/dr-leona-s-alizadeh-50275412b), [7] Dr. med. Christian Booz, Department of Diagnostic and Interventional Radiology, University Hospital Frankfurt (https://www.linkedin.com/in/dr-med-christian-booz-b22b77161).

Any geometric shape of the implant can be displayed clearly. In addition, the literature describes magnesium implants to be significantly less prone to artifact formation than titanium or stainless steel implants (8). Therefore, magnesium alloys are an optimal implant material from an imaging point of view. Since CT is based on X-rays, every examination is associated with a radiation exposure for the patient.

Magnetic resonance imaging (MRI)

Unlike X-ray or CT, MRI does not involve radiation exposure. The physical measurement principle of MRI is called nuclear magnetic resonance and bases on the fact that protons behave like small magnets with a random orientation. Within a strong external magnetic field, such as that of the MRI scanner, the protons align themselves along the magnetic field lines. When energy is added via a high-frequency radio pulse, similar to a microwave, some of the protons change their orientation, leading to a change in longitudinal and transverse magnetization. After the high frequency radio pulse is turned off, the protons return to their original state. The resulting signal can be recorded by the MRI machine and used for image formation. The time required for the realignment along the field lines (longitudinal alignment) is called the T1 relaxation time. T2 describes the signal decay in the transverse plane due to the dephasing of the spins. T1 and T2 times are specific for substances and tissues (9). The image contrast obtained in MRI is based on these differences in T1 and T2 relaxation times and is particularly affected by the time of measurement after excitation (TE, echo time) and the time to re-excitation (TR, repetition time). By increasing the magnetic field strength, the sensitivity, image resolution and contrast of the images produced can be improved. The unit for field strength is Tesla (T). Common clinical MR machines operate at a field strength of 1.5 or 3 T. More rarely, low-field MRI scanners with field strengths of 0.35-0.5 T are used. In research, devices with field strengths of 7 T and more are available (9).

As in computed tomography, one of the major challenges in MRI of metal implants is the occurrence of artifacts. The magnetic properties of metal implants disrupt the homogeneity of the MR scanner’s magnetic field and cause spatial miscoding, distortion, and signal loss or gain. Not only the strength of the external magnetic field, but also the MR-sequence technique used to create the images affects the limitation of image quality due to artifacts. For example, some sequences, such as conventional spin-echo sequences with short echo times, are better suited for imaging metal implants (10).

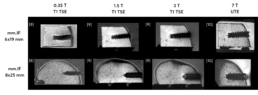

Magnesium is a paramagnetic light metal and therefore suitable for MRI examinations. It is described in the literature that also for magnesium alloy significantly less artifacts occur during MR imaging than for titanium implants (11). In vitro experiments revealed that magnesium implants show excellent imaging properties for field strengths up to 7 T (see Fig. 3).

Figure 3: Comparison of mm.IF interference screws (6 mm left, 8 mm middle) at different MRI field strengths (T) with optimized acquisition parameters in bone specimens. Images by [8] Prof. Dr. med. Hans-Martin Klein, GreenScan GmbH, Burbach (https://www.linkedin.com/in/prof-dr-martin-klein-964252112), [9] Mark Terwolbeck, Department of Diagnostic and Interventional Radiology, University Hospital RWTH Aachen (imaging and article review, https://www.linkedin.com/in/mark-terwolbeck-ba968a159), [10] Teresa Nolte, Institute for Experimental Molecular Imaging (ExMI), RWTH Aachen University (https://www.linkedin.com/in/teresa-nolte-1b9627211).

The image contrast and signal-to-noise ratio obtained improve with increasing field strength. However, also the appearance of artifacts increases with the field strength. Thus, sequence optimization is essential depending on the field strength, the MR sequence, and finally, the implant used. Sequences based on ultra-short echo time (UTE) are particularly advantageous at higher magnetic field strengths, as susceptibility artifacts caused by metal implants can be significantly reduced. Furthermore, T1-weighted turbo spin

echo (TSE) sequences also show good results in initial studies on clinically used scanners with respect to the visualization of magnesium implants at reasonable examination times.

Conclusion

Magnesium is a promising material for orthopedic implants. It is bioresorbable and as alloy it offers similar biomechanical properties as human bone (12). In addition, magnesium alloys are compatible with the most frequently used imaging methods in trauma and orthopedics: X-ray, CT and MRI. There is only little tendency of artifacts generation allowing magnesium alloys to even outperform titanium implants from an imaging perspective.

Literature

- https://www.deutsches-fusszentrum-richter.de/spezielle-methoden-implantate/intraoperative-3d-roentgenbildgebung

- https://www.thieme.de/de/radiologie/artefakte-computertomografie-93044.htm

- https://de.wikipedia.org/wiki/Computertomographie

- https://www.kardionet.de/computertomographie/

- https://link.springer.com/article/10.1007/s00113-016-0232-y

- https://www.universimed.com/ch/article/orthopaedie-traumatologie/schnittbilddiagnostik-trotz-metall-2102650

- https://bmcmedimaging.biomedcentral.com/track/pdf/10.1186/s12880-017-0187-7.pdf

- https://www.die-radiologie.de/kernspintomographie

- https://healthcare-in-europe.com/de/news/ultrahochfeld-mrt-teures-spielzeug-oder-wertvolles-werkzeug.html

- https://www.universimed.com/ch/article/orthopaedie-traumatologie/ schnittbilddiagnostik-trotz-metall-2102650

- https://www.researchgate.net/figure/Artifact-appearance-in-3T-MRI-PDw-TSE-FS-in-two-positions-of-the-screw-0-90_fig5_313731363

- Ezechieli M et al. Biodegradation of a magnesium alloy implant in the intercondylar femoral notch showed an appropriate response to the synovial membrane in a rabbit model in vivo. J Biomater Appl. 2014 Aug;29(2):291-302. doi: 10.1177/0885328214523322. Epub 2014 Feb 12. PMID: 24522242

Conducting Clinical Studies in our New Virtual World

We are delighted to host Pascal Winnen, Founder & CEO of HEMEX, a swiss-based Contract Research Organization (CRO) for this episode in our mm.Blog. Pascal and one of our founders, Florian, give an outlook on how digital tools shape the realization of clinical studies in our new dynamic virtual world.

Given the industries demand to digitalize clinical workflows and enhance clinical data quality and accessibility, how do you describe the state of clinical studies today and in the future?

Pascal: „It may be considered somewhat ironic that the healthcare sector, which is so innovative and fast moving, is still hesitant to embrace the novel virtual clinical trial culture which has now become our reality. The global pandemic has been a driving force in demonstrating how we need to adapt and find new solutions to conduct and monitor clinical trials.

Tools such as Electronic Data Capture (EDC) systems have been instrumental in helping us make the transition to working remotely yet still enable us to collect vital data. EDC platforms allow physicians to enter patient data and for monitors to check that all the information has been recorded correctly. If an error has been made, a quick alert can be raised directly in the system and the problem resolved by the study coordinator. Having access to an EDC platform ensures that everything can be done in real-time and with very high data quality.“

Florian: „From a sponsor’s perspective clinical studies are probably the most complex projects to demonstrate safety and effectiveness throughout the life cycle of a medical device or treatment. Innovation in healthcare currently faces two overlapping challenges. On the one hand, with the MDR in place the requirement for sufficient clinical data has become even more important. On the other hand, the global pandemic creates a big obstacle drastically slowing down site selection, patient recruitment due to postponing elective surgeries, and additional hurdles for source data verification.

Handling the pandemic carves out resources from clinical infrastructure and staff. As time and dependencies always have been a crucial part in clinical project management, any tool that simplifies time consuming workflows involving various parties is a big help. Simple tools such as DocuSign are still not the baseline even though they have demonstrated data security long ago and are commonly used in many sectors.“

How would you describe virtual studies, preferably where does virtual stop and on-site physical presence begin?

Pascal: „There have been many technological advances enabling ‘eClinical’ platforms to establish themselves and assist sponsors, CROs and PIs to all work together virtually. However, work still needs to be done to make these platforms easy-to-use, interconnected and affordable to all those engaging in clinical trial activities.

Ethics Committees have been releasing new guidelines on conducting studies during the pandemic. They will hopefully continue to realize how using technology can enable better, more accurate data capture to support their decision making. There have also been concerns raised over data protection laws and requirements as patient data is entered and stored in locations on the internet.

Going forward, we must work together to establish new norms and standards whilst ensuring clinical trials don’t compromise patient safety and wellbeing. From a legal perspective, electronic signatures, for example, are still not accepted on patient Informed Consent Forms (ICF). In the coming years, this will probably become the new norm and we can all play a role in sharing the advantages and find innovative solutions to prevent misuse.“

Florian: „There has always been a gap between the potential new technologies offer and implementing and realizing their benefits. But when it comes down to the question paper-based vs. digital, the dice have been cast long ago. Today an increasing percentage of healthcare is already engineered, thought and provided digitally. In addition, concepts such as value-based healthcare emphasize patient outcomes and call for more data to track these outcomes along the patient journey. It becomes apparent that clinical studies for innovative treatments incorporating a new ‘digital DNA’ are easier to conduct and monitor virtually.

As interconnectivity in healthcare increases and more clinical data becomes available, data capture and data security are key. Therefore, health authorities and care providers play a crucial role in shaping the ethical and regulatory framework for this evolution. Developments such as ‘smart hospitals’ are fertile ground to innovation in healthcare and more than just a buzzword. Simultaneously, virtual care blends into on-site physical presence, a shift that can already be seen in telemedicine.“

Siteless Trials: Can patients take part in a clinical trial from home?

Pascal: We frequently hear the term ‘Siteless Trials’, which still seems futuristic but is not far from becoming our next go-to method of conducting certain clinical trials. When patients enroll in a clinical study, it can be a daunting process, with many checks, examinations and forms to sign. All these checks are of paramount importance, however, there is scope to improve the patient experience and collect accurate data using other methods which will still support the future successful market launch of the medical device in question.

Using technology, such as wearable devices, could enable physicians to access real-time data collected directly from patients whilst at home. One may ask whether it is really necessary for a patient to travel to the hospital for a check-up 12 months after they’ve undergone a procedure to take their heart rate, blood pressure measurements and have them complete a survey? Putting the patient first when designing trials could encourage more people to participate if there was more flexibility and remote monitoring.

With most patients having access to a mobile device, using apps to collect real-time data is becoming easy. For example, a patient can now effortlessly record an Adverse Event in a couple of seconds on their phone and help patients in the future suffering from similar symptoms or side effects.

Giving patients a ‘voice’ on a platform where they can tell you how they are feeling improves data quality and patient safety. Along the same lines, sponsors can give patients updates via such online platforms to maintain engagement and share the most up-to-date information about their treatment.

Florian: Pascal just outlined the potential benefits that smart devices offer, but many sponsors do not fully acknowledge their added value yet. Sure, they may not be applicable to every medical device or treatment and not every piece of information captured by clicking a button is relevant for the outcome of a clinical trial. However, any technology that enables virtual data capture might add another valuable data dimension that we may have missed in the past or, to some degree, is closer to real world evidence.

“You’re on mute”: Interaction between CRO and Sponsor

Pascal: All-in-all, the global pandemic has made us realize that we can change and do things differently. As a CRO, HEMEX has adapted to our client’s needs and is ready to plan and conduct clinical trials worldwide. We have established a new process, enabling us to conduct Site Initiation Visits with hospital teams virtually. With our colleagues at medical magnesium, we organized a virtual project ‘kick-off’ meeting so that both teams could get to know each other. We have regular weekly meetings to give progress updates and answer any questions, give advice, etc. We hope that we will soon be able to travel to Germany to meet the medical magnesium and the clinical hospital teams with whom we work closely on their two PMCF studies.

All in all, the COVID-19 pandemic has allowed us to reflect and make positive changes. Each and every one of us can now play a small part in transforming the way clinical trials are conducted today and in the future, to make sure that patients are at the forefront of everything we do.

Florian: Conducting virtual clinical studies is an interesting mission statement, especially during the pandemic. At medical magnesium we are at our best in the operating room or wet lab to derive our clinical pathways together with passionate surgeons simply because we are a physical medical device manufacturer. In a post-pandemic time, we will still depend on on-site clinical activities to a high degree and procedures such as arthroscopic surgeries will still be done by highly trained surgeons. Our implants enable a ‘single surgery therapy’ which is closely monitored throughout our PMCF studies. Hence, we would love to invite the CRO team to introduce them to investigators, surgical techniques and corresponding aftercare. As soon as traveling becomes possible again, we will catch up on physical investigator meetings together with our CRO to fully take their experience and perspective into account. In the meantime, we implement digital tools whenever possible.

About HEMEX

HEMEX is committed to changing the future of healthcare by guiding the most promising European start-ups through each and every step to bring innovative pharmaceuticals, medical devices and in vitro diagnostics to the market. Headquartered close to the thriving Basel global Life Sciences hub, the goal at HEMEX is to ensure start-ups have access to a wide range of tailored products, practical solutions and fundraising support, either in-house or via our network of pre-qualified experts, laboratories, CMOs, warehouses, logistic partners and affiliates. This empowers the next generation of transformative discoveries to grow into successful and sustainable businesses, and drive change in both human and animal healthcare. Find more information on www.hemex.ch

Biologics of magnesium as an implant material – mm.X technology insight

The main element of our mm.X implants, Magnesium, as being a metal, shows promising mechanical strength for the use as an implant material quite similar to the human bone. This feature is making it an ideal candidate for different medical devices implanted into the human bone as we have previously discussed in an earlier mm.Blog posting.

But what about the biological tolerability of magnesium as an implant material?

Being an essential element involved in various biochemical procedures, the human body usually contains about 24 g of magnesium, most of it incorporated into and stored within the bones. Interestingly, almost one quarter of all magnesium within the human body is rapidly exchanged within hours between the serum and the extracellular matrix and within few days considering the bone surface pool.1 Excessive magnesium can easily be excreted by the human body, demonstrating its extensive tolerability, while some studies on the human diet even suggest that the average Western diet is lacking up to 300 mg magnesium per day.1

To confirm the tolerability (or: biocompatibility) of the magnesium alloy used for our mm.X implants, we have conducted a battery of biological tests to assess possible adverse reactions which may be caused by the material, including among others inflammatory reactions, cytotoxicity, systemic toxicity, or pyrogenicity. Data from these studies indicate an excellent biocompatibility as there were no signs for suspicious tissue reactions in any of the conducted tests. As the magnesium alloy does neither include aluminum nor nickel, the risk for allergic reactions is further reduced.

In addition, implants from medical magnesium undergo an innovative surface conversion process, transforming the implants’ surface into a ceramic layer. This layer is intended to decelerate the corrosion, the initial hydrogen gas evolution and thus bioabsorption – the key challenge with high-volume implants during the primary post-operative stability phase. By chance, in-vitro data also suggest that the surface treatment further improves the material’s biocompatibility.2

Now, what makes mm.X implants and magnesium particularly interesting in the field of orthopedic and trauma surgery compared to conventional implants?

According to the German Federal Statistical Office, surgeries for “removal of osteosynthesis material” (OPS5 Code 5-787) ranked no. 18 on the list of the most frequent surgeries in Germany. In contrast to conventional metal implants made from titanium or steel, magnesium implants gradually degrade and become absorbed by the surrounding tissue after implantation. This degradation, however, does not occur via an inflammatory reaction as it is the case with polymeric materials but via a physiological process. When the magnesium implant comes in direct contact with the body fluid, the metal oxidates and subsequently dissolves in the presence of chloride ions, an abundant ion within the extracellular matrix.3 Due to this natural biodegradability, removal surgeries may often be avoided by selecting magnesium-based materials instead of conventional metal implants, thereby reducing the overall treatment costs and – most importantly – patient risks and annoyance.4

In addition, magnesium has been demonstrated to not only facilitate wound healing but have osteoconductive and osteoinductive features, thus augmenting the regeneration of bony tissue.5,6 When compared to conventional implant materials like steel, magnesium was found to elevate the expression of genes crucial for the differentiation of stem cells into osteoblasts and thus the formation of new bone tissue. While this study was based on pure magnesium implants, a previous study had already given evidence to a similar behavior of magnesium alloys.7

Hence, we further pursue our mm.X technology to offer more bioabsorbable alternatives to conventional implant materials used in various, but not all, indications among orthopedics and trauma surgery. The beneficial biological, chemical, and mechanical properties make it possible to design highly functional implants together with leading surgeons.

References:

-

Vormann, J. Magnesium: Nutrition and metabolism. Mol. Aspects Med. 24, 27–37 (2003).

-

Jung, O. et al. In vivo simulation of magnesium degradability using a new fluid dynamic bench testing approach. Int. J. Mol. Sci. 20, 1–14 (2019).

-

Han, H. S. et al. Current status and outlook on the clinical translation of biodegradable metals. Mater. Today 23, 57–71 (2019).

-

Farraro, K. F., Kim, K. E., Woo, S. L.-Y., Flowers, J. R. & McCullough, M. B. Revolutionizing orthopaedic biomaterials: The potential of biodegradable and bioresorbable magnesium-based materials for functional tissue engineering. J. Biomech. 47, 1979–1986 (2014).

-

Saris, N. E., Mervaala, E., Karppanen, H., Khawaja, J. A. & Lewenstam, A. Magnesium. An update on physiological, clinical and analytical aspects. Clin. Chim. Acta. 294, 1–26 (2000).

-

Zhang, Y. et al. Implant-derived magnesium induces local neuronal production of CGRP to improve bone-fracture healing in rats. Nat. Med. 22, 1160–1169 (2016).

-

Castellani, C. et al. Bone–implant interface strength and osseointegration: Biodegradable magnesium alloy versus standard titanium control. Acta Biomater. 7, 432–440 (2011).

Author: CP

Value-based Healthcare - Overview, Status and Benefits

In this mm.Blog post, we intend to share our understanding on one of the rising important topics of healthcare industry – value-based healthcare or VBHC. We will summarize and share an overview of why VBHC is becoming more and more popular in recent days. Our insights are based on the research done, through reviews of various literature, online articles and industry insights.

Definition of value in the context of healthcare

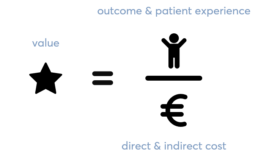

Providing high quality health benefits for every Dollar or Euro spent is one of the most important goals for any healthcare system. Improving patient outcomes is what finally matters. Economic sustainability of healthcare can significantly improve when value benefits can be achieved for patients, payers, providers and suppliers. Value should define the framework for performance improvement in healthcare. Porter ME., 2015 defined ‘Value’ in healthcare as the patient health outcomes achieved per dollar spent.

VBHC is more concerned with quality than quantity of care. It can be defined as a healthcare model based on compensation for outcomes. This system differs from the traditional fee-for-service (FFS) or quantity of care system. In traditional systems, medical providers are on a pay per use type of compensation structure.

Why Value based healthcare is gaining popularity

According to research from Boston Consulting Group (BCG), VBHC approaches deliver higher-quality patient outcomes at the same or lower total cost for a given condition. VBHC is gaining momentum as the proliferation of technologies and capabilities in health care informatics make it possible to collect outcome data and to share the information broadly with clinicians and the public.

Some of the results are:

-

- Patients know with greater certainty which physicians and hospitals deliver better care at the same or lower cost, as well as which drugs, procedures and medical devices would work best for them.

- Payers reimburse based on outcomes and push therapies towards care delivery with better outcomes.

- Providers compete based on achieved medical outcomes, thereby attracting more patients, referrals and payer support.

- Suppliers take a more holistic approach, strategically selecting where to play and what to offer to improve outcomes.

For a successful example one can name OrthoChoice in Stockholm, one of the first big scale bundled payments in the world. In 2008, all major hospitals in the county of Stockholm signed the contract for a bundled payment for low-complex hip and knee replacements. The bundle includes the full cycle of care, from pre-operation to follow-up and complications that occur as a result of the surgery. This way, the bundle rewards reduced levels of complications and infections. (source: VBHC-Thinkers-Magazine 2019)

A comparison of progress across countries

In Europe, Sweden has been named the leading pioneer in VBHC in a study by The Economist in 2015 and 2016. Many organisations are actively implementing VBHC, such as the University Hospital in Uppsala and the Sahlgrenska University Hospital in Gothenburg. Sweden’s national registry has been one of the key drivers.

According to an assessment conducted by BCG for VBHC implementation, Sweden emerged top on list, followed closely by Singapore, while Germany and Hungary came in last. The BCG maturity-assessment framework uses four success factors to evaluate a country’s progress toward value-based health care on two broad dimensions: “Clinical engagement”, “National Infrastructure”, “Data quality” and “Outcomes based initiatives”.

The chart below combines a top-down assessment of a summarized factor national enablers of VBHC (clinician engagement and national infrastructure) with a bottom-up assessment of data quality and use at existing disease registries across 12 major health conditions. It maps countries and their progress in these general factors.

Going into more detail, a country’s performance on each criterion is rated on a scale of 1 to 5, with 1 representing low readiness and 5 representing best practice track success factors, as well as a score for overall readiness, which is the unweighted average of all 35 criteria. In this approach, Germany is at the bottom of the list, owing mainly to limited access to high-quality data and poor data utilization.

The diagram below displays the average score in the four broad categories to track the success factors, as well as a score for overall readiness.

Benefits through VBHC strategy

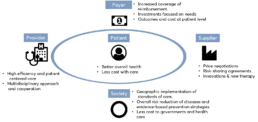

Several benefits come from the introduction of a VBHC strategy to all the involved stakeholders, such as patients, healthcare providers and payers, as well as to society. VBHC models offer better health outcomes to patients, reducing the costs associated with the full-care cycle, such as those related with hospitalizations and use of medical resources. In these models, healthcare providers (e.g., physicians, pharmacists and nurses) are more efficient in delivering and managing patient-oriented care and more likely to engage patients in achieving the recommended goals. In this way, patients could reduce attributable risk factors, through prevention and awareness campaigns, and achieve better early clinical outcomes by receiving early diagnoses and/or targeted therapies. Consequently, healthcare systems are less constrained in terms of costs and the required investments are more realistic and effective, focused on specific needs. The following visualization shows the relations and activities among relevant stakeholders. (source – Redondo, P et al., 2019).

Added value by medical magnesium

Through our product platform mm.X, medical magnesium is contributing to VBHC strategies in collaboration with stakeholders so that more value can be provided to the patients. Our vision is to significantly improve surgical therapy of patients avoiding the gap between the patients’ desire for best treatment and the general focus on cost reduction:

- Improving the quality of care for a target patient population requiring surgical treatment eliminating risks of a required intervention (risk of infection, rehabilitation, time off work).

- Appropriately reducing the costs, growth in expenditures of payors without reducing the quality of care for a target patient population requiring surgical treatment.

The majority of treatments for fractures are currently using conventional metal implants (e.g. plates, screws and nails). These implants used to be made of stainless steel or titanium, requiring a removal surgery in many indications.

With the help of advancement in product research, medical magnesium has introduced the mm.X platform of products based on magnesium technology to combine stability and bioabsorption. The technology makes removal surgeries obsolete, as the fracture gets stabilized to full recovery before the implant dissolves in a controlled manner. In several in-vivo trials, mm.X has shown good results, which indicate a potential rollout to more products. Therefore, we believe in contributing to a VBHC through our mm.X implant technology.

Author: VR/FC

References:

Vos, D.I. and Verhofstad, M.H.J., 2013. Indications for implant removal after fracture healing: a review of the literature. European Journal of Trauma and Emergency Surgery, 39(4), pp.327-337.

Redondo, P., Ribeiro, M., Machado Lopes, M.B. and Gonçalves, F.R., 2019. Holistic view of patients with melanoma of the skin: how can health systems create value and achieve better clinical outcomes?. ecancermedicalscience, 13.

Soderlund, N., Kent, J., Lawyer, P. and Larsson, S., 2012. Progress toward value-based health care: lessons from 12 countries. The Boston Consulting Group, ed. Valuebased Health Care.

Porter, M.E. and Guth, C., 2012. Redefining German health care: moving to a value-based system. Springer Science & Business Media.

Nilsson, K., Bååthe, F., Andersson, A.E. and Sandoff, M., 2017. Value-based healthcare as a trigger for improvement initiatives. Leadership in Health Services.

Porter, M.E., 2008. Value-based health care delivery. Annals of surgery, 248(4), pp.503-509.

We are happy to host Marc Ebinger, Co-Founder&CEO of RIMASYS, a Cologne-based Surgical Education startup for this mm.Blog episode. Together with thoughts of one of medical magnesium’s founders, Kilian, we hope you find a good read on the topic of founding and running a medTech startup in Germany and the German healthcare ecosystem.

You are both based in NRW, RIMASYS in Cologne and medical magnesium in Aachen: Establishing a healthcare startup in NRW, what is your experience? What were your success factors?

Marc: “After living in Cologne for over 10 years I would recommend all young talent to try out the spirit of the open-minded and dynamic Rhineland. In addition to the high quality-of-life, more than 10 million people are living and working in the Rhine-Ruhr area. There is a high density of universities and business opportunities. NRW is very Start-Up friendly. The success factors of our region are the clinical networks here and the vibrant city of Cologne attracting brilliant talents from all over the world. As the Rhine-Ruhr is located in the heart of Europe, we have three international airports which are reachable in less than one hour. We attract healthcare professionals from all around the world developing with us new educational tools and MedTech innovations in our training center CADLAB Cologne.”

Kilian: “Our background spinning out of the RWTH Aachen university combined with the Rheinland mentality, one helps one has been a key element of becoming, what we are right now. We received support by many of the RWTH research institutes, the RWTH innovation and finally the university clinic of Aachen has become a reliable partner. The high level of education and availability of applicants for open positions, from a skilled manufacturing engineer to PHD in neurobiology at our Aachen location, was and is a crisp success factor. This enables us to build up our smart and pragmatic team at medical magnesium around the translation of latest research into surgical theatres.

Biomaterials take long breath as bio absorption needs to be validated in long term efforts. You only have one shot, as any other development cycle takes too long. Aside from collaboration with the University, I would name the collaboration among the endless list of strong MedTech companies in NRW a success factor. Even If competitive, we established partnerships with a mindset of: Big ocean – lots of fish, there is room for many trawler, which I believe in personally.”

What is your take on German healthcare in worldwide competition? If you could forward one message to Mr Jens Spahn what would it be?

Marc: „German healthcare is more and more under cost pressure. Due to the DRGs hospitals need to shorten operation time. Additionally, keeping with the work time law surgeons in training have reduced hours used to train procedures in the OR. Thus, less number of cases and routine. This has the impact of lowering quality of skills and therefore increasing costs for post-treatment of unsuccessful operations. Every patient should have the right to get treated by experienced surgeon. With all the simulation possibilities, hands on training should be outsourced from the operation room like in other disciplines. Such as the aviation industry where pilots learn all relevant skills in a flight simulator. Training and simulation must be reflected in the DRGs and surgeons need support for outsourced training simulation without risking the patient’s outcome.“

Kilian: „The German healthcare market is characterized by a very low-price level, but high volumes compared to other countries in the EU. Compared to the US or Japanese market, it catches few economical industry attraction. But there is an astonishing number of medical experts, so industry focuses on education and convincing opinion leaders of their respective technology, with a possible fast rollout in the language cluster Switzerland, Austria, and Germany. Therefore, the German market is still of significant importance for most companies.

There is another very important characteristic of German healthcare. My message to Minister Spahn would be: Establish new and speed up existing reimbursement routes for more cost-effective patient treatment with evident clinical data. The German reimbursement system leads to a low price level, but at the same time prevents fast spreading of innovative patient treatment as very long procedural time schedules and a lack of clear responsibilities have become routine. For example, a resorbable trauma implant for children surgery with a possible total cost benefit (through eliminating removal surgery) takes several years for a general reimbursement route after it has stated its clinical effectiveness.”

Kilian, medical magnesium is producing medical implants with a very “hardware” based business model. How do you compare the German Medical technology Center Tuttlingen and your location in Aachen NRW for a medical device start-up?

Kilian: „Tuttlingen has an incredibly experienced workforce and know-how at the companies there. Sometimes it is hard to identify the right partners because most of the knowledge is not marketed and intangible. As medical device company, we have reliable partnerships with a network of companies around Tuttlingen. They offer support in many of our „daily“ requirements as an implant manufacturer.

Still, I would not consider relocating or opening a branch in Tuttlingen. Our approach at mm, sometimes naive, helps to pursue and further develop ideas with a very open minded and young team. Tuttlingen and the impressively successful companies there already lack skilled young professionals, probably mostly reasoned in its remote location and beautiful nature. Accessing and collaborating with companies in Tuttlingen from our base in Aachen, with all the benefits I mentioned above, seems to be the best pick for medical magnesium.“

Marc, the RIMASYS group is further looking into digital business models around surgical education, such as your Surgical Island platform. If you think through internationalization, is opening a US entity in the Silicon Valley an option for you or would you prefer more traditional clinical hotspots such as Boston or Houston with the impressive TMC infrastructure?

Marc: „We will always keep our roots in the vibrant city of Cologne as all our team enjoys the Kölsch lifestyle and the openness of the culture here. As the US market is in our focus over the next couple of years, we are already building up all the basic infrastructure and partnerships to address the special needs of the North American market. We would prefer more the clinical hotspots as the intense and dynamic work and the close collaboration with all the Healthcare professionals is in our DNA. To become the Go-To platform for surgeons and healthcare professionals we need the digital talents. Surely it is not just the Silicon Valley where we can offer them a harmonious working and living culture.“

About RIMASYS

Rimasys GmbH is a technology-driven health-tech start-up, founded as a university spin-off in 2016. Core of the Cologne based company are proprietary biomechanical algorithms describing injury mechanisms, utilized to generate lifelike fractured anatomical specimen with closed soft tissue mantle. Rimasys is focusing on enhancing surgical education and improving patient outcomes by advancing practical skill training and medical device development. Further innovation is focused on digital health, artificial intelligence, and virtual reality. The growing team of 35 young and ambitious professionals is aiming to build a disruptive eco-system of solutions at high pace enhancing surgeon education and interaction. For more information, visit www.rimasys.com

Planning and performing clinical studies in times of COVID-19

Clinical studies are an important tool to generate clinical data during medical device development and its time on the market. The data being generated and declared as clinical data are safety and performance data of the medical device. Prior to CE certification, these data are required to demonstrate the conformity with certain regulatory requirements. However, even after the product has been placed on the market, manufacturers are obliged to actively collect clinical data for vigilance purpose to further surveil the product’s safety and performance initially demonstrated in a pre-market situation. These post-market clinical data reveal the product’s safety and performance during regular practice and allow to identify and evaluate undiscovered risks to continuously update the benefit-risk assessment over the device’s entire life cycle. One way to actively collect clinical data under real-life conditions is to carry out Post-Market Clinical Follow-up studies (PMCF studies).

The current pandemic has a profound impact on the planning and preparation of clinical studies. In order to successfully run a clinical study in times of COVID-19, sponsors have to think about alternative strategies and spend increased effort on forward planning.

Increasing digital networking activities

To conduct a clinical study, one of the first tasks is to recruit participating study sites. Conferences and symposia are particularly important for attracting medical partners and building up a network. They offer a good opportunity for manufacturers of medical devices to present their products and to meet physicians and important key opinion leaders in person to establish valuable contacts. In times of the corona pandemic, such events are impossible and were converted into a digital format. Even though this new format is now well accepted, it offers only limited networking possibilities. In order to provide adequate information and to facilitate networking, we make a special effort to present ourselves well on social media platforms and on our company’s website. To proactively expand our network of clinical partners, we continuously contact promising clinics and investigators by phone or e-mail to introduce our company, our products and (pre-)clinical research activities. Furthermore, we established the possibility to be actively contacted using research@medical-magnesium.com if there is an interest regarding to a cooperation or participation as a clinical study site. We come back to requesters as soon as possible.

Overcoming limitations due to travel and visitation restrictions

Due to the limited travel and visitation possibilities, personal on-site meetings in clinics to present study projects or discuss study questions are also highly restricted. Fortunately, digital meeting formats also offer a remedy here and are actively used by us. However, travel and attendance restrictions also affect ongoing clinical studies. For example, study subjects may no longer be able to attend to the planned data collection visits, and clinical monitors may no longer be able to visit the study centers. The latter must verify that the study is being conducted and data collected properly as part of on-site quality assurance. Although the presence of study subjects is required for certain examinations by the investigator at the study center, we recommend remote monitoring whenever possible to best ensure data quality independent of on-site visits.

Of course, study subjects might also be infected by Covid-19 or must be quarantined as a precaution. An infection impairs the health of the study participants, may affect generated data and prevent further participation at the clinical study. A quarantine might also prevent the subject from participating on planned study visits at this time. As a result, Covid-19 has a strong influence on data quality and the completeness of data sets.

Whenever possible, we thus recommend obtaining study data from quarantined subjects by phone at the scheduled time if no medical examination is planned as part of this study visit

How to deal with surgical restrictions

Due to the ongoing pandemic, many employees in hospitals must carry out new medical tasks in order to provide sufficient care for the large number of corona patients that are admitted and require appropriate treatment. This is accompanied by the postponement of non-essential surgeries to save resources, especially affecting clinical studies with implants intended for sport injuries as these kinds of surgeries are often postponed. Thus, study relevant data are not collected in the scheduled time. In addition, the massive restriction on team sports might reduce the incidence of certain sports injuries in the light of further patient recruitment. In order to achieve the best possible recruitment rate, we therefore recommend recruiting enough study centers to reach the target number of study participants within a reasonable period of time.

Consider an impaired rehabilitation of patients

Finally, there is also the risk that essential post-operative rehabilitation and physiotherapy after surgery may be impaired by corona restrictions. Manufacturers who initiate clinical studies in times of COVID-19 and whose data to be collected may be affected by inadequate rehabilitation measures, should take this into account. Hence, we suggest the possibility to inquire whether the rehabilitation of the study participant was carried out as intended for the respective indication or not. This information will help to interpret the collected data correctly.

With the help of these alternative methods and approaches, Sponsors might be allowed to plan and conduct clinical trials in the best possible way by successfully counteracting some of the major limitations caused by the COVID-19 pandemic.

Author: CC

MDR moratorium: A halftime report

In 2017, the European Commission has agreed on and published a new regulatory framework for medical devices to substitute the present Medical Device Directive, thereby increasing the scrutiny on medical device manufactures and supply consistent and practicable rules EU-wide.

In the beginning, the MDR was often understood as a major burden for both established and new medical device companies due the increased requirements for pre-clinical data and post-market surveillance. Originally, manufacturers of medical devices were given a three year transition period until May 26th 2020 to duly adapt their internal processes and products to the new regulation.

During the transition period, however, it became clear that the MDR is not only a challenge for manufactures, but that notified bodies and competent authorities themselves encountered a variety of obstacles as well leading the entire transition onto a rather rocky road. In late 2019, only a small fraction of notified bodies was designated for MDR due to a significant delay within the designation process. The MDCG (Medical Device Coordinating Group) was also way behind their schedule for relevant guidance documents intended to clarify and substantiate the European Commission’s expectations on how to follow the new rules, and the European database for medical devices (Eudamed) seems to be delayed by a matter of years even. And then: Covid-19.

European Comission deciding for a 12 month extension

As a result, the European Commission decided to extend the transition period by one year. This extension period has now reached half time, but still: only 17 out of 48 notified bodies that have applied for designation until recently have actually been designated yet.[1] In addition, although quite a number of guidance documents has been published already, the list of guidance documents under development is constantly growing. While there were 30 MEDDEV guidelines available under the MDD, more than 40 MDCG guidances have been published up to now – some of them have already been revised – and another 36 documents are currently on the schedule.[2] In summary, it appears that a lot of open questions and uncertainties are still to be addressed even half a year after reaching the original MDR-deadline.

Logically, the Medical Device Regulation (MDR) has been the main topic among medical device manufacturers from all divisions for the past years now and with its implementation still in progress, the debate on how the elevated expectations for quantity and quality on clinical data will actually affect the industry still lives on. Of note, the transition from MDD to MDR comes with considerable costs for established manufacturers not only in regard to the time and personnel required for implementing the changes, or the increased service fees from the notified bodies, but especially in regard to the revised general safety and performance requirements (formally: essential requirements). A recent survey from a German EDC service provider indicates that medical device companies spend approximately 5% of their annual revenue for MDR compliance alone.[3] It has thus often been feared that a considerable number of products will drop out from the market – especially those for orphan diseases and rare conditions – for their manufacturers to cope with the rising costs and that innovation of new products decelerates due to this increased level of required clinical data, making the life especially difficult for young businesses and start-up companies.

Our approach at medical magnesium

Being founded in 2015, our team at medical magnesium was faced with the upcoming regulatory changes early on. We implemented the future requirements into our current procedures, anticipated the need for sufficient clinical data on our MDR projects early on and allocated our resources accordingly. This allowed us to dynamically render our process to the respective needs and shift our focus even on short notice. Half-time through the transition, we thus managed to achieve our first main goals as a medical device company on the fly by receiving the CE mark for our first devices under the MDD. Our believe in procedural dynamics and open discussion among all company departments (from development to clinical affairs) allowed us to anticipate the MDR moratorium early on and specifically guide our resources onto certain projects to speed up the process of product validation and certification. As a result, we had been able to draft and submit the complete technical file for our latest mm.X implant, the mm.CS, early before deadline and have finally received the CE mark for our third class III implant.

Being able to achieve these goals during this rather turbulent time of MDR transition and the ongoing health crisis not only fills us with pride. It lets us believe that small business can certainly stand their ground in the MDR regulated medical device market and allows us to face the future confidently.

Author: MG

[1]https://ec.europa.eu/health/sites/health/files/md_newregulations/docs/notifiedbodies_overview_en.pdf

[2]https://ec.europa.eu/health/sites/health/files/md_sector/docs/mdcg_ongoing_guidancedocs_en.pdf